For millions of adults considering graduate school—and parents planning college for their children—the financial equation is changing dramatically. With major federal student loan reforms taking effect in 2026 and 2027, the way Americans borrow for higher education will never be the same.

If you’re wondering, “Should I go back to school right now?” or “Is borrowing for college still worth it?”—you’re not alone. As your Friend–Expert, I’m here to help you unpack the emotional decision-making and navigate the facts clearly and calmly.

This educational guide walks you through whether returning to school still makes financial sense, what alternatives exist, and how the upcoming federal changes must shape your planning.

Key Takeaways

- Major federal loan changes begin July 2026, including elimination of Grad PLUS loans.

- New borrowing caps may limit access to high-cost degrees.

- Parent PLUS loans will have strict annual and lifetime limits.

- Deferment and forbearance options will shrink beginning 2027.

- Borrowing for part-time enrollment will be prorated.

- Schools can set lower program-specific loan limits.

- Borrowing can still be worth it—if your program’s ROI is strong and your borrowing aligns with the new limits.

- Alternatives like scholarships, payment plans, employer support, and community college matter more than ever.

The Biggest Question: Is Borrowing for School Worth It Anymore?

Short answer: It depends.

Long answer: It depends far more than it used to—because new federal limits will restrict access to large loan amounts.

Before making any decisions, you need to evaluate:

- Your earning potential after graduation

- The program’s cost vs. new borrowing limits

- Your current financial stability

- Alternative training, certificates, or employer-sponsored options

And now—the new 2026 federal rules must be part of your calculation.

Major Federal Student Loan Changes Coming in 2026–2027

These changes affect anyone searching for phrases such as:

- “Are Graduate PLUS loans going away?”

- “New federal student loan limits for 2026”

- “Parent PLUS loan changes for 2026”

Let’s break them down in plain language.

1. Graduate PLUS Loans Are Going Away (July 1, 2026) ❌

This is the most significant change for future graduate and professional students.

✔ Graduate PLUS Loans will be eliminated for new borrowers.

Students already enrolled before July 1, 2026 may continue using the old limits—but only for that same degree program.

This matters because Grad PLUS currently allows students to borrow up to the full cost of attendance. Without it, borrowers must stay within new capped limits.

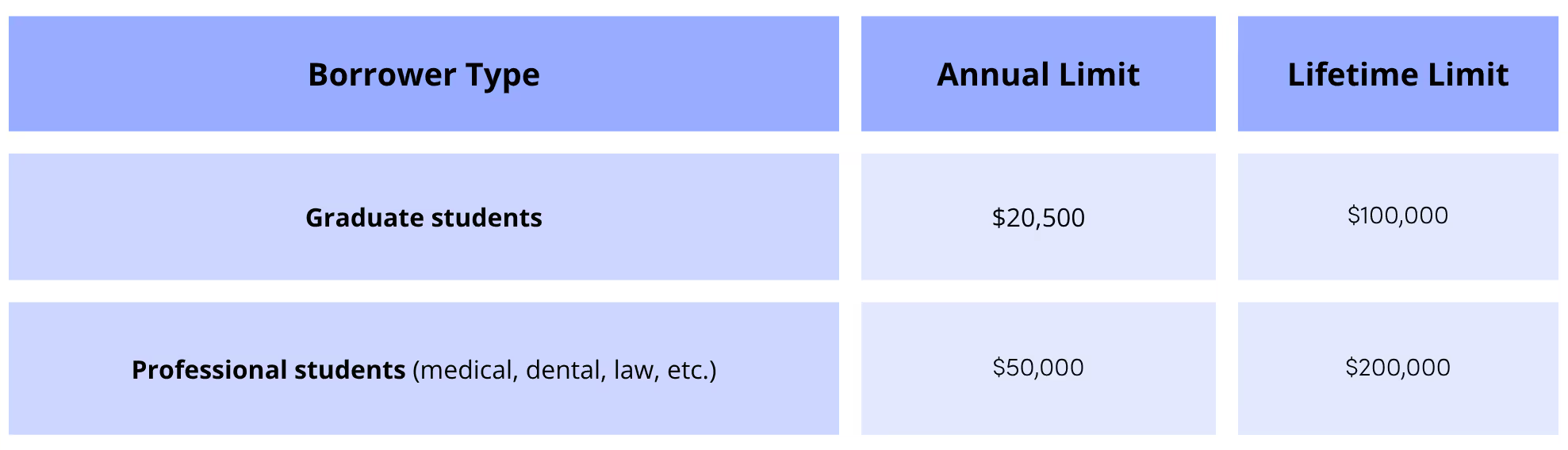

2. New Borrowing Caps for Graduate & Professional Students (Starting 2026) 📉

These caps mean that high-cost programs—MBA, medical, dental, law, and many STEM degrees—may require cash savings, employer sponsorship, scholarships, or private loans to cover the gap.

Purpose of the new rules:

- Reduce overborrowing

- Slow tuition inflation

- Encourage schools to be more transparent about real costs and outcomes

3. Parent PLUS Loans Will Also Be Capped (Starting 2026) 👨👩👧

Currently, parents can borrow unlimited amounts up to the full cost of attendance.

That ends in 2026.

✔ New Parent PLUS Caps:

- $20,000 per year per child

- $65,000 lifetime limit

Parents who want to remain eligible for income-driven repayment (IDR) must consolidate before July 2026.

This is why search terms like “how to avoid Parent PLUS loan debt” are skyrocketing in 2025.

4. New Federal Lifetime Borrowing Limit: $257,500 (2026) ⛔

Beginning July 1, 2026:

✔ Lifetime federal loan maximum (excluding PLUS): $257,500

This combines ALL undergraduate + graduate borrowing.

Students enrolled before July 2026 can exceed the limit only if they stay in the same program.

5. Deferment & Forbearance Options Are Shrinking (2027) ⏳

Borrowers commonly search for:

- “student loan deferment rules”

- “can I get unemployment deferment?”

Beginning July 1, 2027:

❌ Unemployment deferment disappears for new loans

Allowed only for loans disbursed before July 1, 2027.

❌ Economic hardship deferment ends for new loans

Same deadline.

❗ General Forbearance Tightens

For loans disbursed after July 1, 2027:

- Only 9 months allowed in any 24-month period

Borrowers will need sustainable repayment strategies, not repeated pauses.

6. Part-Time Student Borrowing Will Be Prorated (2026) 🎓

Loan eligibility will be based on the percentage of full-time enrollment.

This directly affects common searches like “Can part-time students get federal loans?”

Part-time enrollment = smaller loans.

7. Colleges Can Set Lower Loan Limits by Program (2026) 🏫

Schools may reduce borrowing limits for programs with:

- Lower expected salaries

- High completion risk

- Lower economic mobility

They must:

✔ Apply limits equally

✔ Give students advance notice

✔ Demonstrate financial justification

This is intended to prevent overborrowing in low-wage career paths.

🧭 So… Is Going Back to School Still Worth It?

It can be—if you evaluate your return on investment more carefully than ever.

Ask yourself:

✔ Will this degree significantly boost my earnings?

Search term: “how to calculate the true cost of graduate school”

✔ Can I complete the program within the new borrowing caps?

If not, what’s my plan for funding the gap?

✔ Am I eligible for PSLF or employer tuition assistance?

Search term: “how to qualify for Public Service Loan Forgiveness for graduate school loans”

✔ Should I enroll before July 2026 to preserve current borrowing options?

This matters if your program is high-cost (MBA, medical, dental, law, PT, OT, pharmacy, engineering).

🌱 Alternatives to Borrowing Heavily (Now More Important Than Ever)

1. Community College Pathways

Search term: “is community college a good financial decision for adults returning to school”

2. Scholarships for Working Adults

Search term: “scholarships for adults returning to college”

3. Tuition Payment Plans (0% Interest)

Search term: “college tuition payment plan options for families”

4. Part-Time or Online Grad Programs

Search term: “best part-time graduate programs for working adults”

5. Employer Tuition Assistance & Loan Repayment Support

Search term: “companies that offer tuition reimbursement for graduate school”

❤️ The Emotional Side: Your Future Matters

These federal changes may feel overwhelming, but you’re not alone. Whether you’re planning your own graduate degree or helping your child prepare for college, you’re ultimately searching for stability, purpose, and opportunity.

And that is worth navigating carefully.

Before deciding to borrow—or return to school—make sure you understand how the 2026–2027 federal changes affect your personal situation. Speak with a financial wellness expert who can help you build a smart, personalized education plan.

Your future should empower you—not overwhelm you. 💛

.png)